A "How To" On Discounted Cash Flows

How I Use DCFs To Determine Value

Several of my previous articles have centered around explaining to my subscribers how to establish if a stock they are looking at is a buy, a hold, or a sell. In “Welcome to my Newsletter: The Value Road” I talked about reducing your investment risk by buying into companies with a large net asset valuation and relatively small amounts of debt. In “Finding Value Where Others Can’t” I explained how companies with small market caps can often fit this description because large investment firms are oftentimes not looking at these companies specifically because of their small size. In “Bottom Fishing” I wrote about how investors can often find bargain stock purchases in companies that are going through some sort of difficulty resulting in an erratic share price slump. Lastly in “Hidden Asset Values” I described scenarios which can result in a company having asset values far in excesses of what is suggested on their balance sheets due to GAAP accounting policies.

I believe wholeheartedly that these investment philosophies, when practiced faithfully, can help investors from every walk of life significantly grow their wealth. Before I ever bother to take a closer look at a company these principles mentioned in the four articles above are what pass through my head. If the company under the microscope seems to have the right combination of value investing criteria, I will then proceed to construct a discounted cash flow.

A discounted cash flow analysis is simply a way for an investor to attempt to estimate how much money a company can generate for its shareholders. If after taking into account all of the company’s future expenses and then dividing that net cash flow by the company’s outstanding shares, that value is substantially greater than the company’s current share price, you may have a stock that’s worth a buy. While I find DCFs to be at times indispensable, cash flow analyses by their very nature will leave an investor with no choice but to make assumptions about the future of a company. It is for this very reason that I perform a DCF at the very end of any analysis I perform on a company after I have had a chance to absorb all of the more “matter of fact” elements surrounding the business.

Even if I were to put more weight on a DCF than I do, I would still have to finish my meticulous readings of all of the company’s 10-Ks, 10-Qs, press releases, and earnings releases. Sometimes just a couple of sentences from one of these papers will be enough to skew the end result of a DCF. It is for this reason specifically that I always try and look at any DCF as supplementary data to be used in conjunction with other relevant information and not as the sole determining factor of someone’s investment.

Where to Get Your Financial Information

For no other reason other than to be able to show my readers a lot of information in one neat image I am pulling the financial information for this DCF from Seeking Alpha. This is purely to avoid having to insert a ton of images into this article which in turn would make my article too large and messy to be able to send out in a single newsletter as this is a rather in depth topic. I highly recommend that whenever you pull financial data for a potential investment that this data gets pulled directly from the SEC’s or company’s website. Although Seeking Alpha’s financial information is almost always correct, I have in a couple of very rare instances (for a couple of very small companies) found inaccurate or slightly outdated data. The best way to steer clear of this in my experience is to rely solely on data that comes straight from the source and that has a large legal obligation to be correct.

In order to provide an example to use for our discounted cash flow today, we will be looking at the Butler National Corporation Inc. (OTCQX:BUKS)

Getting Started on a Discounted Cash Flows

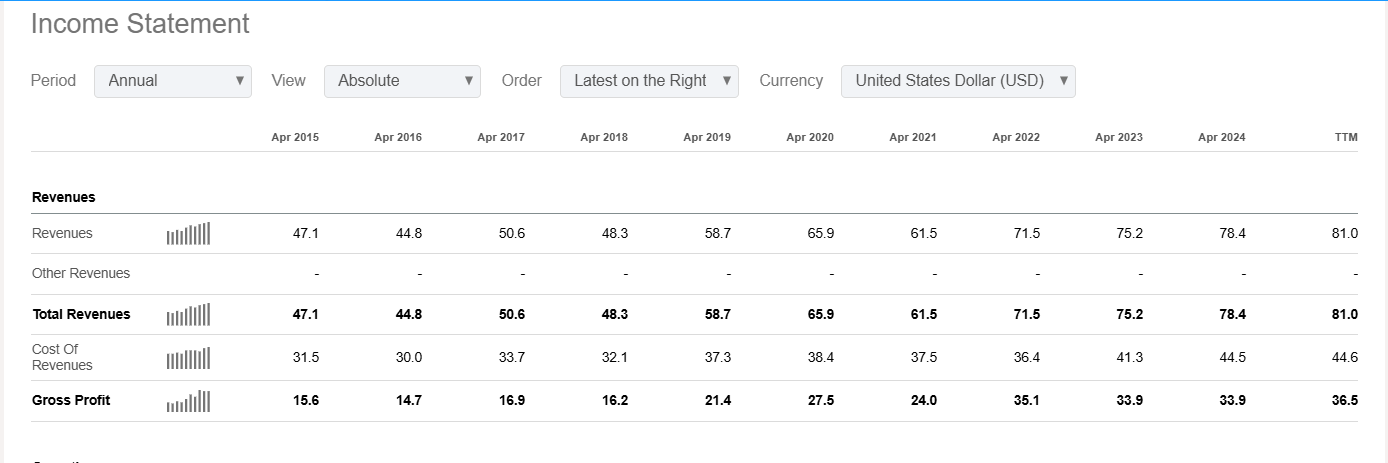

In order to get a better look at whether or not BUKS has enough of a cash flow potential to warrant a buy rating we must start off by taking a look at the company’s revenues.

If we focus on BUKS’s revenues from 2020 to 2024 we can see that the company’s revenues rose from $65.9 million to $81.0 million. That’s a 22.9% increase over that time period. That works out to an average increase of 4.58% in BUKS’s revenues each year during that period. If we average out BUKS’s revenues year over year we get a slightly higher average revenue growth rate of 4.8%. Simple differences in determining the average growth rate of a company such as this can sometimes lead to large differences in the end value of a DCF.

Normally I use the year over year average growth rates for my DCFs however I do take into consideration both of these methods for getting an average revenue growth rate for a business that I’m looking into. Large one year increases or decreases in growth can sometimes skew year over year growth rate averages more than just averaging out the gain between the start of a period under consideration and the end of that period under consideration. The COVID-19 pandemic is for many companies, the perfect example of huge changes to year over year figures that have the potential to change their average growth rates much more than averaging out the gain between the start of a period and the end of that period under consideration.

For this reason I urge caution when putting together a cash flow analysis. I would also urge my readers to make sure they are able to understand the limits of using a DCF. If your year over year growth rate average is 15% from 2020 to 2024 and the growth rate you come up with when you average out the difference between 2020 and 2024’s revenue figures only amounts to an 8.0% growth rate, you’re gonna to have to start thinking critically.

Is the business I am looking at likely to keep up this unusually high rate of growth for an extended period of time? Sometimes the answer is yes. New technologies that have never before been available to the public can experience very large and prolonged periods of growth. The revenue growth rate of a TV company during the first five years that Television sets had first become available was usually massive but slowed down significantly as soon as those with means to obtain a TV had obtained one. While the invention of the TV was around a hundred years ago, this growth principle holds true today. Tesla has seen a 2,937.0% increase in revenue since 2014. While I do not doubt that Tesla has a good chance of experiencing another impressive decade of growth, the odds that the company could experience another 2,937.0% increase in revenue is astronomically low. That would put Tesla’s revenues at $2.8 trillion.

This is why I urge a bit of extra caution when it comes to forming your DCF. A large part of investing is simply having reasonable expectations concerning the company’s you are invested in. If you are the type of person that gets easily excited about a large jump in revenue or a substantial increase in a business’s margins I would be extra skeptical of your early DCFs. I would even urge you to step away from your computer for a day and come back with a fresh and clear head to take a second glance at your work.

I personally do all of my stock research late at night and I do not use price limits. This forces me to buy or sell my shares during a normal trading day so the option of being able to act impulsively on an investment is largely avoided. Safeguarding yourself against impulsiveness when it comes to investing has been just as an important part of my investing success as has learning about all of these other value investing principles. If you can’t force yourself to slow down enough to utilize the knowledge you’ve learned to make better decisions, then you kind of just spent all of that time learning all of this stuff for nothing.

Back to BUKS

Revenue Growth Projections

Concerning BUKS’s future revenue growth predictions. BUKS is mostly an aerospace company that also operates a casino. The company had an excellent year, growing their revenues by 15.4% year over year during the first quarter of the company’s fiscal 2025. While it is promising to see a company’s year over year figures increase by so much, judging a single fiscal quarter to another single fiscal quarter gives us a very limited insight into a company’s revenue figures. It is for this reason that I will be assuming BUKS’s full projected 2025 revenue figures to be only 8.0% above last year’s revenue figures before normalizing the company’s revenues to a growth rate of 4.8% from 2026 through BUKS’s fiscal 2034. If BUKS is able to grow their revenues at this rate, in 2034 the company will see its revenues hit $129.1 million.

EBIT Margin Projections

Next we’ll move on to BUKS’s EBIT margins.

EBIT is the revenue from a company with the cost of goods sold and operating expenses subtracted from it. EBIT can sometimes also be referred to as operating income. From BUKS’s fiscal 2020 to their fiscal 2024 their EBIT margins averaged out to be 14.6%. While it actually appears that BUKS’s EBIT margins have been sustainably improving higher than this, I am still keeping the company’s projected EBIT margins at 14.6% in an attempt to remain conservative about the overall growth prospects of BUKS. If the company is able to maintain an EBIT margin of 14.6% through their fiscal 2034 then their EBIT figures should grow to approximately $18.85 million.

Are These Projections Reasonable Expectations For A Company?

Now would be a good time to bring back up the point of using extreme caution when putting together a DCF. In the case of BUKS it is entirely believable that a business like this would have the ability to grow its revenues from $78.4 million to $129.1 million over the course of a decade. If however I noticed that BUKS’s revenues had tripled or quadrupled during that time period I would have cause to double check my math and then seriously consider the likelihood of whether or not a business like BUKS could really grow that fast over the next decade.

Is this company about to sign some sort of massive contract? Is a particular business operation they are involved in growing at a pace that suggests growth of this kind is possible? The answers to these questions may be yes but… I would just make sure you are confident that whatever growth catalyst you have factored in when analyzing a company’s future cash flow is not just a realistic possibility but an overwhelming probability. Getting too excited about unrealistic expectations will lose you a lot of money.

Factoring in Average Tax Rates and Capital Expenditures

Now that we have BUKS’s revenue and EBIT margin projections down we can factor in the company’s average effective tax rate. From BUKS’s 2020 to their fiscal 2024 the company saw an average tax rate of 23.5%.

I will then subtract this tax rate from each of the company’s EBIT figures from 2025 through to 2034. After factoring in BUKS’s projected tax expenses, I will then move on to the company’s average capital expenditures expense.

I factor in these expenses as a percentage of the company’s revenues. In BUKS’s case their average capital expenditure expense as a percentage of the company’s revenues was 9.9%. When adding this expense to BUKS’s cash flow projection year by year, we start at an expense of $8.5 million and then progress to a $13.2 million expense by BUKS’s fiscal 2034.

Adding Depreciation and Amortization Expenses Back Into BUKS’s Cash Flow Analysis

After BUKS’s capital expenditures have been subtracted from the company’s post tax figures we can move on to the company’s depreciation and amortization charges.

I actually add these charges back into the company’s cash flow figures. D&A charges are not costs to a business in the same way that other expenses are. D&A is simply money put aside to replace the cost of a company’s assets over time. We are adding these expenses back into our DCF because these expenses are just cash that the company holds onto in order to be able to purchase more assets at a later time. Since the entire point of a DCF is to figure out how much cash a company will generate to be able to grow its business, putting D&A charges back into a company’s yearly projected cash flows can help us get a better look at all of the cash a company could have available to put to a productive use in the future.

D&A expenses can often stay the same for years at a time before increasing all of a sudden. This is because company’s can often buy assets in spurts leaving high D&A costs as a percentage of a company’s revenues initially before that percentage rate drops back down over time as a company finds new revenue sources to be able to run these new assets nearer to full capacity which in turn, increases the revenue of that company. Over time though, these figures often even out. You can actually see this happen with BUKS. From 2014 to 2019 the company’s D&A expenses sat between $3.4 million and $4.0 million before experiencing an 88.0% increase in 2020. What happened? BUKS simply obtained more assets to continue on its business.

BUKS’s average D&A charge was 8.4% of their revenues between 2020 and 2024. When looking at BUKS’s D&A projections through 2034 we begin our 2025 projection by adding back in $7.1 million worth of D&A expenses and by 2034 those expenses are projected to sit at $11.2 million.

Accounting For Working Capital

Lastly we have to factor in how much of an increase in working capital a company will have to invest in to be able to grow their business. Working capital is the difference between a company’s current assets and its current liabilities. As a company grows in size it needs to put more of the money it makes aside to be able to continue to fund its current operations. Whatever a company adds to its net working capital I subtract from a company’s cash flow. I do this because every dollar a company needs to spend in order to be able to make money is a dollar that can’t be considered free flowing cash specifically because it has a specific purpose that is needed to continue a company’s operations.

When a company finds a new more efficient way of running its business, or perhaps has some type of pricing advantage that will let them continue to grow revenues without having to invest in expanding their facility or machinery to continually increase their production, that business may show decreases in their working capital. When this happens the value of this difference can actually be added back into a company’s cash flow statements. Different businesses have very different working capital requirements and I would recommend paying attention to a company’s change in net working capital closely as it can be an indication of how much more expensive a company’s operations may be as they expand.

When we take a look at BUKS’s change in net working capital from 2020 to 2024 they had a total decrease over that time period of $3.5 million.

Divide that by five and we get an average decrease in BUKS’s net working capital of $700,000 a year. For my net change in working capital estimates I decreased the company’s working capital from 2025 through 2027 by $700,000 a year before increasing their working capital as a percentage of their revenue by 10% from 2028 onward.

We have now considered all of the factors that I look closely at when constructing my DCFs. I estimate all of these figures out from 2025 through to 2034. After adding or subtracting all of these factors into a company’s cash flow for each year from 2025 through to 2034 we are left with what is called a company’s unlevered free cash flow. Now we have to add a discount rate…

What is a Discount Rate?

The next thing we have to do is add a discount rate to each of these yearly projections. A discount rate is a calculation that investors use in order to better account for the risk of lending out their money to a business. Obviously when an investor gives his or her money to a company they are expecting a return on their investment. If you plan to invest $10,000 into a stock for a year, you can’t use that same $10,000 to invest in something else during that time period. You can only spend your money once right? If a better investment pops up during that time period and you’ve already committed that money to another investment, you’ll just have to let that opportunity pass on by. A discount rate is also a way of accounting for the possibility that your investment might actually do much worse than you had forecasted. In the vast majority of cases the smaller or more volatile the company that you’re investing in is, the higher the discount rate will be when attempting to forecast that company’s free cash flow.

Essentially a discount rate is a way of adding a tangible cost to “waiting for a return on your investment” by reducing a company’s unlevered free cash flow figures by a percentage that compounds year by year to reduce the value of a company’s cash flow in direct proportion to not just how long you would have to theoretically wait for that return but also for how much risk you are taking while that money is invested in that company.

The percentage you use to account for the risk you are taking waiting on an investment to produce an adequate return could differ rather widely from investor to investor. While many investment philosophies view small market caps as an enhanced risk, I believe that there can actually be a lot of safety investing in small companies that have a large surplus of assets. I usually do not add additional percentage points to account for a company’s small market cap unless they are so small that I may actually have a hard time finding a buyer for my shares.

Full disclosure, I am not rich, not even close. I work a normal shitty job in an industrial manufacturing facility while trying to grow my wealth through the virtues of investing knowledgably and through living my life with a healthy dose of frugality. The positions in my brokerage accounts usually have a value of somewhere between $1,500 and $4,000. The only stocks that I have ever had a hard time selling due to the company’s size all had market caps under $30.0 million. If you’re fortunate enough to be able to throw $40,000 into a position, your ability to able to sell off those shares quickly should the need arise may be very different than my ability to dump $4,000 worth of stock from that same company. That is however part of the beauty of only having relatively modest amounts of money to invest. You can buy and sell your shares from these smaller companies much more easily than larger investors can. This means that you have an ability to find out about these undervalued companies before multimillion dollar funds can.

How I Normally Determine My Discount Rates

While discount rate percentages can vary widely from one investor’s analysis to another most fall in between a 10.0% to a 12.0% range. These ranges change for numerous reasons other than a company’s market cap such as the interest rates on US treasuries, the business sector that the company operates in, current company problems, and so on and so forth. My normal starting percentage for my discount rate is usually 10.0%. This is a way to account for the higher risk you would be assuming investing in one of these stocks versus the probable return you would likely be receiving if you just put your cash into an S&P 500 Index (SP500) over the course of someone's investing lifetime.

My rational for this is… Why spend all of this time looking into companies that aren’t likely to outperform the market? If you could make just as much money letting your investment sit in an S&P 500 index fund as you could reading a bunch of financial information and doing a bunch of math then you should just invest in an S&P 500 index fund. If it looks like you could make way more than that investing in a company you’re looking into however, then all of your work could be very worth your while.

Adjustments to this 10.0% discount rate will then be made depending on various factors I have usually learned about while reading through the company’s 10-Ks and 10-Qs. If it looks like I might have a hard time selling my shares, I will probably add another 2.0% to the discount rate. If management is constantly issuing stock and diluting the company’s cash flow per share I might add on another percentage point. If the sector this business operates in is extremely volatile like say oil or natural gas, I might add on another percentage point or two to that discount rate.

Putting the Discount Rate into our Discounted Cash Flow

For BUKS I will be leaving the company’s discount rate at 10.0%. In order to add a discount rate to your projected unlevered cash flow figures from 2025 to 2034 you’ll need to follow this formula. If math is not your strong suite you may also find this link very helpful.

where:

CF1=The cash flow for year one

CF2=The cash flow for year two

CFn=The cash flow for additional years

r=The discount rate

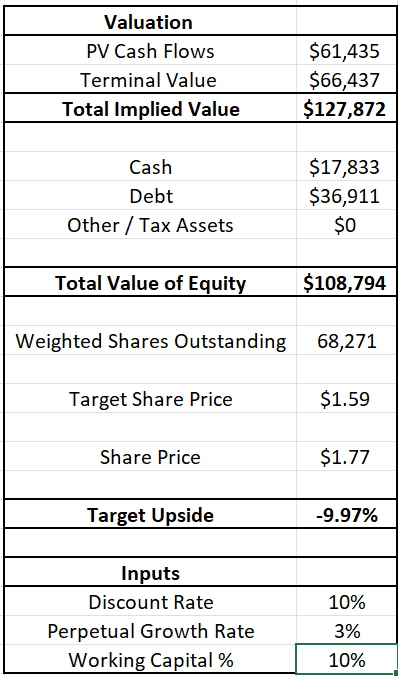

Once we apply our discount rate to BUKS’s unlevered free cash flow figures we can see how significantly it reduces the company’s cash flow value with each additional year that it is applied to its cash flow. For our 2025 figures I projected that BUKS would have an unlevered free cash flow value of $8.8 million. After factoring in our 10.0% discount rate that cash flow value gets lowered to $8.0 million. If we fast forward all the way to our 2034 unlevered free cash flow projection for BUKS of $12.3 million and factor in that compounding 10.0% discount rate, it reduces the cash flow value of that year down to just $4.7 million. Once I have applied this discount rate to all of BUKS’s future unlevered cash flows from 2025 through 2034 I add all of those figures up to get BUKS’s present value of their future cash flows, which in this case comes out to $61.4 million.

Next we have to calculate the terminal value of BUKS’s cashflows. This is to account for all of the cash flow value that a company is likely to produce from the final year of our projected cash flow until “the end of time”. The equation for this is

FCF / (d – g)

Where:

FCF = free cash flow for the last forecast period

g = terminal growth rate

d = discount rate

Taking into Account BUKS’s Terminal or Perpetual Growth Rate

As you’ll notice this equation requires something called a terminal growth rate. The terminal growth rate or perpetual growth rate as it is sometimes called, is just the rate at which a company will likely grow at once it matures past our initial cash flow forecast period and into a slower rate of growth. This rate is usually between 1.0% and 3.0% depending on the type of business and the industry in which they operate in.

Right now would also be a perfect time to add that a company’s perpetual growth rate will likely never be much higher than the average GDP rate of the country they operate in. The average rate of GDP growth in the United States has been 3.0% since 1948 but has slowed down as the United States has become a more economically mature nation and I would expect it to remain under a 3.0% annual growth average going into the next 50 plus years. For this particular DCF I put BUKS’s terminal growth rate at 3.0%. When running this through our terminal value equation I produced a terminal value figure for BUKS of $66.4 million.

Adding in the Rest

Once we have the terminal value and the present value of BUKS’s cash flows we can add those figures together to get BUKS’s total unlevered cash flow value of $127.9 million. Now we have to add into this value the $17.8 million worth of cash from BUKS’s balance sheet as well as subtract from this value the company’s total debt burden of $36.9 million. This finally gives us the total value of the company’s cash flows while also accounting for all of the company’s debts it has yet to pay as well as all of its cash on hand.

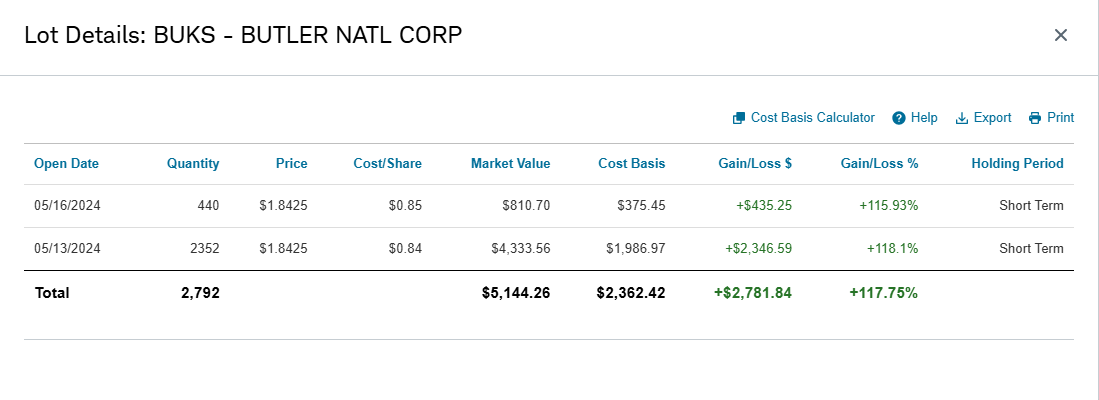

This total levered value for BUKS comes out to $108.8 million. When we divide that number by the company’s 68.3 million outstanding shares we get BUKS’s cash flow value per share which comes out to $1.59. When comparing that to the company’s current share price of $1.77 we can actually see that BUKS is currently overpriced by about 10.0%. I had bought this stock at $0.84/$0.85 per share and it appears that now it may be time to sell.

Why and When to Sell

BUKS’s current net asset value looks to be sitting around $0.82 per share. When I bought into the company the stock sat at about $0.84 per share. As mentioned in my newsletter “Hidden Asset Values” a company will often have property or buildings that would be worth far more sold off today than their GAAP value would suggest and essentially at the time BUKS was fairly valued on a net asset basis with a very large cash flow value upside. This is why I bought into BUKS in May of 2024. Now that the stock price has risen far above the company’s net asset value safety net and is hovering around being somewhere between fairly valued and slightly overvalued on a cash flow basis, my reasons to hold onto BUKS no longer exist.

This here is an important part of investing and perhaps the hardest part to learn. People have a very hard time getting rid of a stock, especially one that has made them so much money. This leads us to one of the most important questions in investing. When do I sell my stock? To know when to sell a stock you have to first know why you bought that stock in the first place. If you bought a stock because it had a large net asset value, a large upside potential in cash flow value, and was then experiencing a price slump, you should sell that stock when the company no longer has a large cash flow value upside and when the stock price has risen above its slump and has surpassed the company’s net asset value.

In the case of BUKS the company is now overvalued or at the very best fairly valued on its future cash flows and is now very overvalued on a net asset basis. For these reasons I will be selling my BUKS shares. I will however likely wait until I have held onto them for a year for tax purposes. I will however, be keeping my eyes peeled for potential developments that could put any downward pressure on the stock in the meantime.

Disclosure: I am long Butler National Corporation Inc. (OTCQX:BUKS) and will buy or sell my shares anytime following this article. This is not financial advice. I am not a financial advisor. Do your own research.