Finding Value Where Others Can't

A Focus on Smaller Capitalized Stocks

Where to Look for Undervalued Companies

Hello readers and welcome to another addition of The Value Road. As you’ll recall from my very first letter, our first rule for the stock market is an echoing from the one and only Warren Buffet and his number one rule. “Don’t lose money in the market.” This rule is much easier to repeat than to practice. Investing in companies with an ample amount of assets and little to no debt is the first step to protecting yourself from losing your investments. This was covered in my first newsletter in great detail with an in-depth look at Alico, Inc. (NASDAQ:ALCO). Today I would like to help our readers find stocks that fit this description on their own.

How do you find a stock that has a ton of assets with little or no debt that is still underpriced on a net asset basis? Obviously, you could (and should) keep reading these newsletters to get the scoop on opportunities in the market but there are other ways to find stocks that are potentially underpriced if you know where to look. Contrary to most investment philosophies, I believe the best way for the average person with modest amounts of capital to invest, is to invest in small, micro, or Nano-cap companies. Let’s take a minute to discuss why people dislike small businesses so much.

What’s Bad About Small Business?

Negative connotations to investing in companies of this size usually revolve around an investor’s ability to enter or exit out of their position in a timely manner. This can be a real concern, especially when investing in small over-the-counter companies trading on pink slips. It is important to look at the trading volumes of companies before purchasing a stock. If a company only has a theoretical average trading volume of 100 shares per day and you buy 500 shares you won’t be able to offload your stock in one day because there will very likely not be a buyer on the other end of that transaction to purchase the shares you are trying to sell. If a company is small enough and you are rich enough to own a very large position relative to the amount of total shares the company has outstanding, when you sell your position you will likely drop the share price, in turn dropping the profitability of your investment.

A Contrarian Philosophy About Business Size and Investment Safety

The reasons why it is hard to offload large positions all at once happens to be the same reasons why investors of more modest means can thrive in spaces like these. Hedge funds can’t buy into these stocks the same way that individual investors can because of the small trading volumes. If you own 10% of a company’s shares you get a seat at the board. This means that if a $1 billion hedge fund wanted to purchase $10 million worth of shares from a company that has a $100 million market cap, they would have to allocate resources to help run that company, resources that cost a hedge fund (or anyone for that matter) money. Even if a hedge fund made a 30% return on its investment that is only a $3 million gain. That $3 million is only a 0.3% gain for the hedge fund. While a 30% return looks amazing in and of itself, a $3 million gain against a $1 billion portfolio ends up as just a 0.3% gain. That’s just a drop in the bucket. That drop gets even smaller once you subtract all of the time and resources that the hedge fund spent fulfilling their role on the board.

Small Size Can Be A Guard Against Large Hedge Funds

From my experience the unwillingness for larger hedge funds to be able to invest in these smaller companies leads to a stock performing more in line with its actual business performance and less in line with how one hedge fund decided to trade. Large companies attract investors with an enormously diverse range of incentives that may or may not be tied to the actual performance of the business under consideration. The modern-day investor is very interested in Bollinger bands and Whipsaws or what they think broader market sentiments entail. This sort of security analysis is in my opinion, much more speculative than basing a stock purchase off of whether a company is engaged in a well-run and profitable business venture.

The Influence of Hedge Funds on Other Investors in the Market

While these large hedge funds can create discrepancies between the value of a business and the price of its shares, retail investors can and are now exacerbating this discrepancy. It is basic human psychology that people seem to have an innate fear of missing out, especially when they are missing out on getting rich. This leads a lot of investors to play a game of follow the leader in the market.

When a hedge fund buys or sells a position in a company that is large enough to create a significant price change, many other investors will follow suite and buy or sell their shares. Much of the time an investor isn’t doing this as part of some larger portfolio strategy but just because an influential investor or fund did it. Sometimes these buys or sells happen automatically as the modern investor can automate at what price their shares get bought or sold at. This can create a large chain reaction based off of the actions of a single hedge fund and may not even correlate to the reasons why that specific hedge fund sold off their stock in the first place.

This is why I invest in small companies specifically. Tech companies with multi-billion dollar market caps can bleed money for years at a time and their share price can still go up while another company with a multi-billion dollar market cap can run a profitable business and see its share price stagnate just because the business is viewed as “boring”. When you invest in companies that, by their very size, would exclude most hedge funds from being able to distort a company’s share price away from its actual business performance, you increase your chances of realizing predictable gains based specifically on a company’s operations.

Be Selective When Picking Your Investments

People will often bring up the poor average returns on smaller stocks. There is also a general worry that small cap stocks will have a harder time surviving economic downturns. While it is true that small cap stocks have underperformed large cap stocks on average in recent years, I am not advocating that you purchase ETFs or index funds that cover a wide array of stocks.

An enormous amount of small cap stocks are biotech companies. The biotech industry is full of companies that take on enormous amounts of debt for research and development projects that often never create a new saleable product. This in and of itself can skew average growth rates for small cap stocks as a whole. Being very selective and not broadly investing in small companies will ensure an adequate return on capital for an astute value investor that knows what to look for. If you invest in companies that have little to no debt with ample assets to sell in the event of an economic downturn, then the argument that small cap stocks have a harder time surviving economic downturns as compared to larger cap stocks holds no weight. Again, it is very difficult to file for bankruptcy while being debt free.

There are various forms of stock screeners available on the internet, usually for free that can prove to be an invaluable tool for helping an investor find an underpriced stock. I use the Charles Schwab screener personally but most will do just fine. I would recommend looking for companies under a $500 million market cap. If you run into companies with a market cap under $250 million, all the better. I would then personally exclude all biotech companies and then look for companies with a low price to book ratio and that have a lot of assets and little debt. From this point on you can begin to read their 10-Ks and 10-Qs. With a bit of diligence and patience you will begin to find some companies that have the potential for some market beating gains.

An Example of a Company with a Small Market Cap, Lots of Assets, and Relatively Little Debt

Net Lease Office Properties (NYSE:NLOP)

In November of 2023 a company called W. P. Carey Inc. (NYSE:WPC) wanted to get rid of some of its office real estate. The result was a spin off called Net Lease Office Properties (NYSE:NLOP).

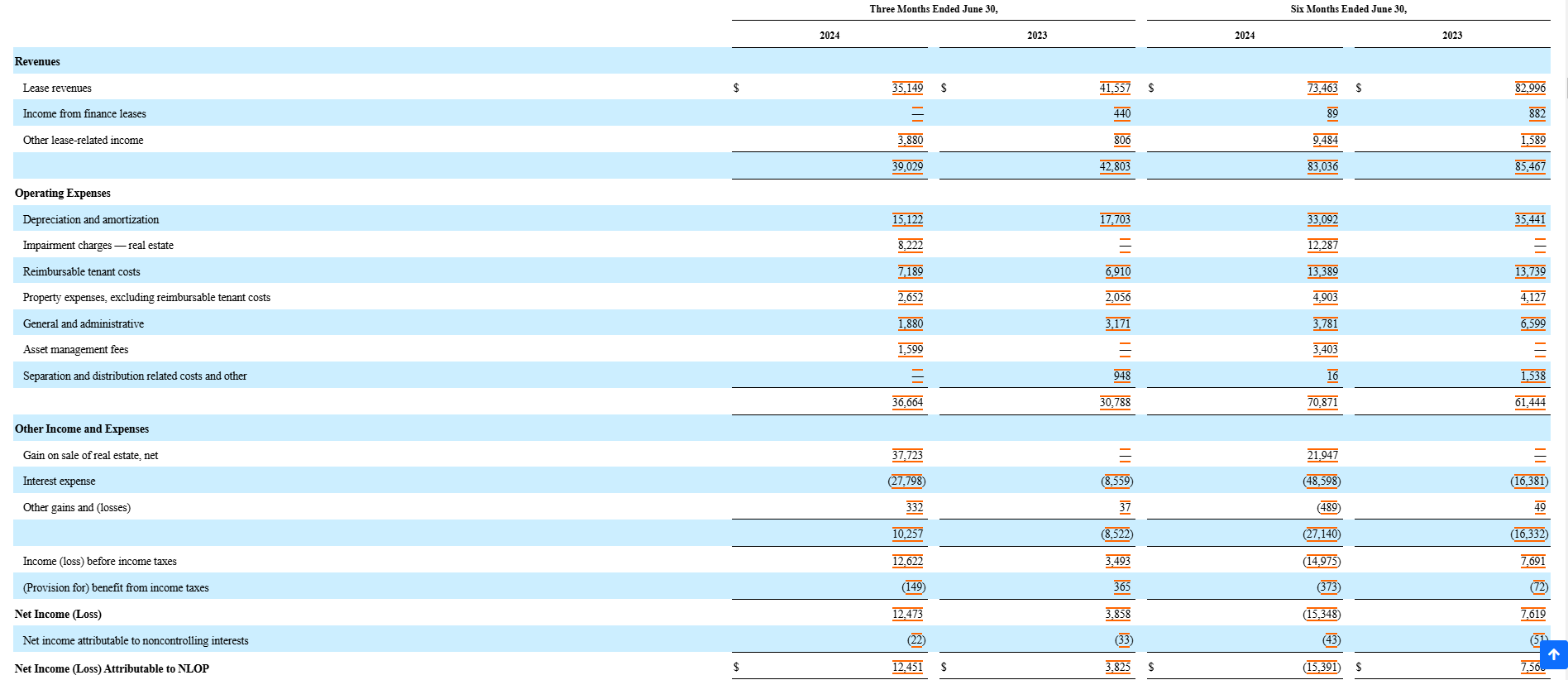

While NLOP does have $327.4 million in debt as of their most recent 10-Q, the company has been selling off its real estate assets in order to rapidly pay this debt down. NLOP is the perfect example of a company that has a large amount of assets that it is currently selling in order to pay down its debts very rapidly. The company had $1.31 billion in assets in December of 2023 and had as of their last 10-Q, sold eight buildings for $236 million leaving NLOP with $1.04 billion in assets. This shrunk NLOP’s debt down from $541.98 million in December of 2023 to $327.4 million as of June 30th, 2024.

As of August 8th, 2024 the company sold off another building for $71.5 million bringing up total proceeds from building sales for NLOP to $308 million. The company used these proceeds to pay back another $63 million worth of its outstanding debt which should drop the company’s debt down to somewhere in the range of $264.4 million. Provided this estimate is accurate, so far within just the first eight months of the year NLOP was able to cut its debts by 51.2% and still has over $1 billion in assets to sell off.

NLOP’s Ability to Become Profitable From Operations

NLOP has a real potential to generate positive net income from its operations. The net loss of $15.39 million the company has shown in its first six months of its fiscal 2024 can be attributed to two factors that NLOP is feverishly in the process of eliminating. The first is NLOP’s large $48.6 million in interest payments. NLOP cut their debt by 51.2% this year and as the company continues to make progress with this endeavor their interest expenses will shrink. This is more than enough to push NLOP into profitability.

The other factor preventing NLOP from generating income is the company’s impairment charges on their real estate. These charges reflect the difference in an asset value as it is currently valuated and the actual estimated value that asset would fetch should it be sold off in today’s market. Because some of NLOP’s buildings had dropped in value as the COVID-19 Pandemic reshaped the demand for office space, the company had to observe this drop in value as an expense on its income statement. This expense (which is not an expense the company would have to use its cash to pay for) makes up 79.9% of NLOP’s net loss for the first six months of the company’s 2024. Once the company has finished paying down its debts to a much more satisfactory level NLOP will probably stop selling off its assets, will no longer suffer these impairment charges, and will finally begin to realize the full potential of its operational revenues.

During the three and six months ended June 30, 2024, we recognized impairment charges totaling $8.2 million on two properties and $12.3 million on four properties, respectively, in order to reduce their carrying values to their estimated fair values, which approximated their estimated selling prices.

- NLOP’s 2024 Q2 10-Q

After NLOP’s debt payments show signs of significant reduction their interest payments will begin to fall. These falling interest payments coupled with the absence of further real estate write downs should improve the company’s income statements drastically. This will likely be a catalyst to send the stock price rising further. NLOP’s share price may even rise as soon as NLOP posts their 2024 Q3 10-Q showing that the company used the $71.5 million in building sale proceeds to pay down more of their debt as this was only announced in a press release and not in a SEC filing.

NLOP’s Net Asset Value

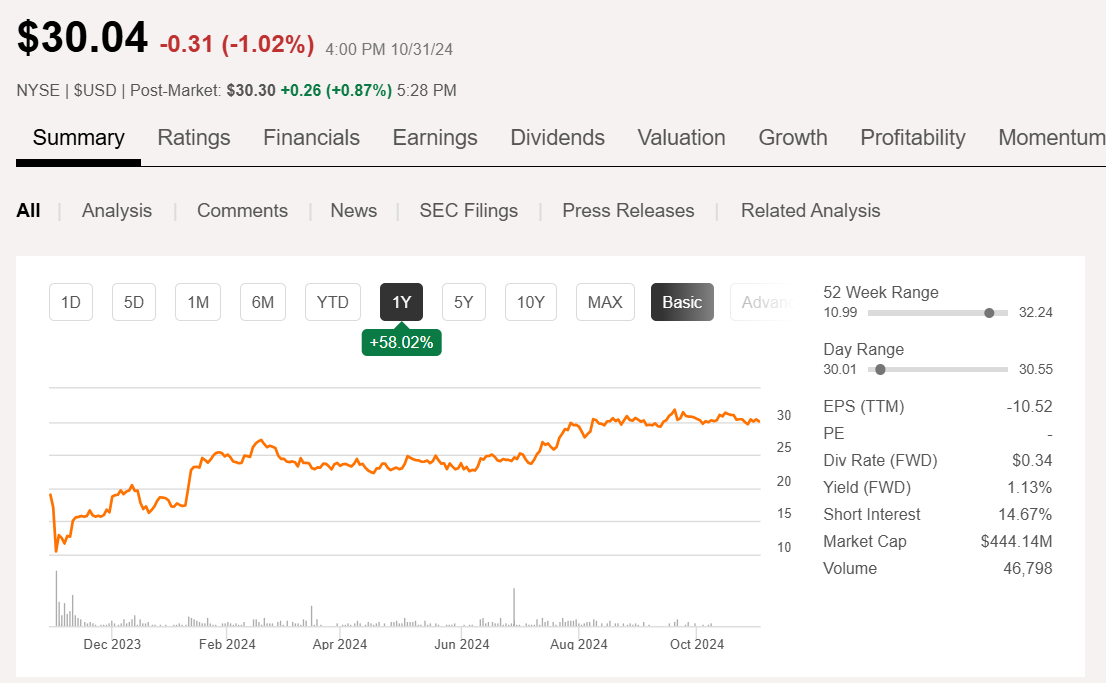

Since NLOP has yet to post a 10-Q that encompasses the $71.5 million the company received for its latest real estate sale, I will assume for this net asset valuation the company’s figures from their 2024 Q2 10-Q. After subtracting the company’s $380 million in total liabilities from their $1.04 billion in total assets we get a net asset value for NLOP of $664.6 million. If we divide this value by the company’s outstanding share count of 14.79 million we get a net asset value per share of $44.95. That’s a 48.1% increase from the current share price of $30.35.

Conclusion

I believe that NLOP is a BUY as long as the company continues to chip away at its debt at a meaningful rate in order to shorten the length of time the company has to spend recording write downs on its real estate properties. These write downs make the company’s business performance appear far worse than it actually is. While investors have enjoyed a good share price return from NLOP since its introduction as its own business entity, once this REIT spin off gets its chance to return to normal operations, I think that the stock price will shoot up even further once the company’s financial statements become much more easily digestible for everyday investors to pick apart.

Disclosure: I am long Net Lease Office Properties (NYSE:NLOP) and will buy or sell my shares anytime following this article. This is not financial advice. I am not a financial advisor. Do your own research.