Hidden Asset Values

Assets Hidden by Accounting

Hello readers of The Value Road. I have recently published three other letters that each go over an important concept in value investing. The titles of these letters are “Welcome to my Newsletter”, “Finding Value Where Others Can’t”, and “Bottom Fishing”. These writings go over how to find a company small enough to significantly negate the risk of that stock being influenced by one or two large hedge funds, with little to no debt, and a net asset price per share that’s significantly higher than the stock price. If this business is also experiencing some sort of downward trend and the price of its stock is near some sort of historic low point, then you very well may be looking at a stock that’s a buy.

In today’s letter we will be expanding upon the concept of picking companies with a surplus of assets large enough to make the physical value of the company worth more than the current share price. Most of the time this kind of surplus in asset value is very apparent on a company’s balance sheet. When it becomes obvious that a company’s asset values overshadow the current share price, investors will often swoop in and begin to buy up the stock raising the share price, possibly beyond the point of the stock being a bargain.

How does a normal person stumble on these bargains before the rest of the market finds out about them? Sometimes you can just get lucky and stumble upon a stock that’s beaten down with ample value before the rest of the market catches on. Sometimes you can buy into a stock as its share price is crashing in value due to some negative publicity that’s separate from the performance of the business. Sometimes this negative force is a lawsuit that may dish out some bad news and unwanted expenses but is likely nothing that would substantially effect a company’s normal operations.

I have bought into stocks under these scenarios. When these opportunities arise, be ready. I oftentimes however, buy into companies that have “hidden asset values”. These usually stem from Generally Accepted Accounting Principles (GAAP) that can in some instances, mask how much a company’s assets are really worth. Sometimes these GAAP policies can make a company overstate its liabilities.

In my own investing adventures, a company’s buildings and property are the most likely thing on a balance sheet to be severely undervalued. This is because these assets last a long time and usually appreciate in value substantially. GAAP accounting however, states that a company must record this land value at cost. Every millennial has heard the bit about “Boomers” buying their house in 1971 for a ridiculously small sum of money only for it to be worth $1 million today. This concept is no different in business.

The Maui Land and Pineapple Co Inc. (NYSE:MLP), a company we’ll be talking about in greater detail a little later in this newsletter, is the perfect example of GAAP accounting hiding a company’s true property values. According to MLP’s last 10-K their land value was recorded at $5.05 million. They own 22,300 acres of land in Maui, HI. The average cost of land in the contiguous United States is about $12,000 per acre. If MLP sold off that land at just $12,000 an acre they would receive $267.6 million. In West Maui, the particular area where the company owns the majority of its property, the average price for an acre of land is easily north of $1.5 million. The difference in total land value between just $5 million and $267 million is jaw dropping let alone MLP’s actual land valuation which is close to $2.0 billion.

The reason for this monstrously large discrepancy in land value is due to MLP purchasing this land between 1911 and 1932. That $5.052 million that the company has recorded as the value of this property works out to just $226 an acre. When a company has massive differences between the real value of their assets (especially assets likely to be sold off) and the stated value of their assets, the company’s share price will often times not take into consideration this hidden asset value at all. Once a business begins to sell off these assets or put them into productive use, it catches the eye of investors.

In many instances this becomes a catalyst to a rapid rise in the company’s share price. This sudden interest from other investors garnishes the interest of even more investors and all of a sudden the market decides that it wants to factor in these hidden asset values. Patience and sound analysis are two very important factors when investing in companies with hidden asset values. Sometimes the market finds out the hidden value of a stock you’ve been looking at rather quickly, sometimes a couple of years will go by before the company begins to take advantage of its assets in a way that finally catches the attention of other investors.

Sometimes a company’s net asset value is depressed by things that show up as liabilities but are not actual costs that a company would have to absorb with its own resources at a future date the same way it would with other liabilities. Deferred income is a common example of this phenomenon. When a company has accepted payment for a product or service that it has not yet delivered it cannot count that money as cash on its balance sheet. These payments instead go to a deferred income row on the liabilities portion of the balance sheet. While it is true that a company is absolutely liable for that money until they have completed their part of the business arrangement, that money can’t be touched until the product or service is delivered. If the money has to be returned to the customer, that liability would be simply erased from the liabilities section of the balance sheet. The company would not have to use its cash on hand or take on debt to service this liability. When liabilities such as this appear on a balance sheet it can help to obscure the true value of a company’s assets. This kind of liability doesn’t usually skew a company’s asset value nearly as much as carrying the value of land or buildings at cost but it is always something to factor in when looking through a balance sheet.

MLP: A Great Example of a Business with a Ton of Hidden Assets

Maui Land & Pineapple Company, Inc. (NYSE:MLP) is the perfect example of a company that at first glance seems to have a relatively unspectacular balance sheet. While the company’s $41.9 million in assets according to GAAP accounting still far surpasses the company’s $7.7 million in liabilities, when you divide out the company’s $34.2 million in net assets by the company’s 19.65 million shares outstanding we get a small $1.74 worth of value per share. That’s a 92.8% downside from MLP’s current share price of $24.30. If you were to scroll past this company and do a bit of quick math to see how much of a margin of safety you would get should you buy into MLP, I wouldn’t blame you for skipping over this investment opportunity.

As discussed previously in this newsletter, MLP is an example of a company who, through following basic GAAP accounting procedures, are forced to carry the value of the land they own at cost. As is evident to anyone who’s turned on their T.V. over the past couple of years, the price of everything has risen dramatically. In MLP’s case they began buying land in Hawaii in 1911 and continued until 1932.

This brings me to the main concept of this newsletter. MLP began purchasing its properties over 100 years ago way before Hawaii was even a U.S. state. Hawaii now not only has its statehood but has become a prime destination for both tourists and wealthy Americans who are looking to hold assets in paradise. This has made the price for an acre of land in Hawaii dwarf the average price of an acre of land in most places in the United States and puts the state in the top 5 for most expensive places to buy land in the country.

Land on the island of Maui is even more expensive and in West Maui, where most of MLP’s properties are specifically located, even more so. In mid October I looked up the cost of land in Kapalua and averaged out the price per acre for all nine properties that were up for sale at the time. While the price of each lot depended on multiple factors, the average cost per acre in Kapalua came out to $1.73 million. That’s an extreme appreciation in value compared to the $226 per acre average that the company had originally purchased the land for and still has to use as the value of its land on its financial statements. Just to put that number into perspective, the value of some of MLP’s properties increased by as much as 766,414.6% from what is written down on their balance sheet.

While most of MLP’s properties are located relatively close to its Kapalua resort, the company does own 1,463 acres in what is referred to as “Upcountry Maui”. When I looked at 39 separate land parcels in the area they averaged out at a much smaller $664,642 an acre. MLP is in the process of selling 30 of these acres as ranch lots. MLP is also working on planning a community on some of this land. Their 2023 10-K states

We own approximately 1,463 acres in Hali‘imaile zoned for agriculture, light industrial, and business which is in the federal Tax Cuts and Jobs Act (“TCJA”) Opportunity Zone. Our landholdings include 290 acres classified for growth potential as “Small Town” in the long-range County of Maui Island Plan. As of this filing, we are underway with master planning for all land in Hali‘imaile. - MLP’s 2023 10-K

Now that we have some ball park figures on what the land in the areas in which MLP owns property are selling for, we can start to put together a more accurate representation of what MLP’s land is really worth.

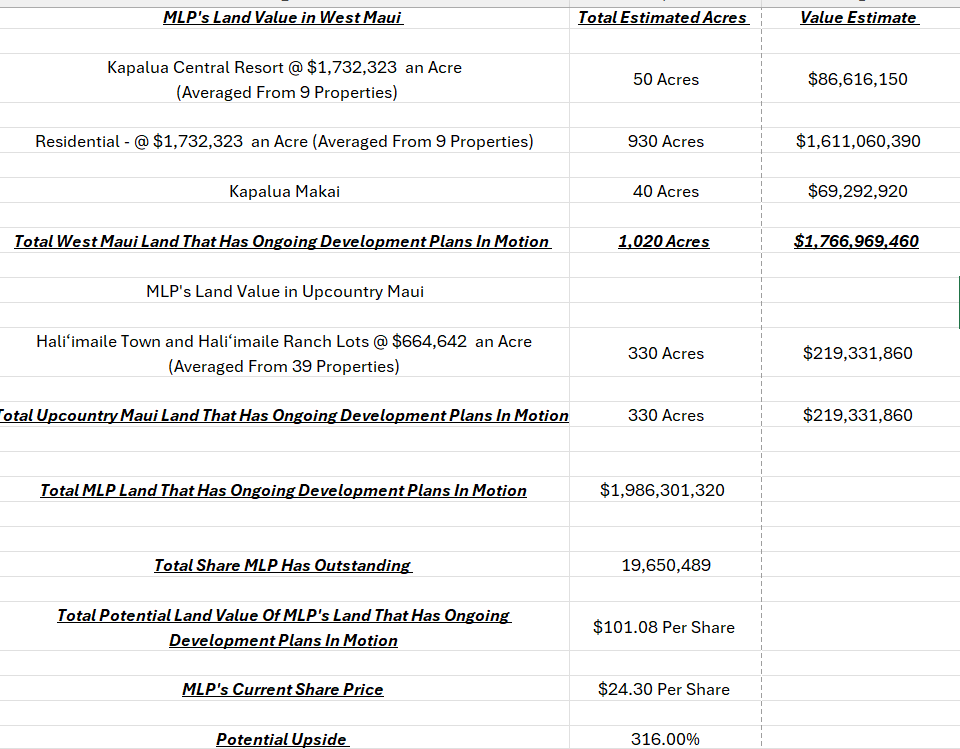

Here are what MLP has reported to be their active development projects as of December of 2023. In my model of MLP’s land value estimations I did put down an additional 290 acres in MLP’s Hali’imaile development projects as management has specifically talked about building housing on this property.

As you can see from the chart above MLP could rake in close to $1.77 billion just from their planned 1,020 acres of mostly residential developments in West Maui. When you divide that by the company’s 19.65 million outstanding shares, you end up with $89.92 worth of value per share. That’s a 266.3% upside from the company’s current share price of $24.30. When we add in the additional acreage of the company’s Hali’imaile properties into the equation we end up adding an additional $219.33 million to MLP’s potential property value, approximating $1.99 billion in total. Dividing that figure by MLP’s outstanding shares gives us an approximate property value of $101.08 per share, presenting a 316% upside from MLP’s current share price.

While it may take some time to realize this value I believe that as management starts to complete building projects, and rake in the massive revenues waiting for them from selling off their land to do so, investors will begin to hear about these profits. Building projects in Maui can prove to be extremely difficult due to having some of the most extensive building regulations in the nation. In most cases this is a bad thing but this may actually play into MLP’s favor. In recent years the company has added to its management roster some of the most talented builders nationwide and over the course of many of their careers have built many award winning communities and resorts.

More importantly a lot of these new faces have extensive experience building on Hawaii. This should help smooth out Hawaii’s regulatory process for MLP while simultaneously helping to keep out competition from other potential land owners looking to develop their properties.

In August of 2023 Maui suffered a terrible tragedy from wildfires that scorched the town of Lahaina and much of the west Maui area. While none of MLP’s properties had been damaged a lot of areas south of the company’s properties had been very badly effected. This has put pressure on the government to speed up Hawaii’s grueling regulatory process for building. This could help MLP but may actually help the company’s competition more as businesses without the managerial know how of MLP’s CEO and board members may be able to build housing faster than they would otherwise be able to. As of October Hawaii’s Governor Josh Green extended an emergency proclamation to help build housing in Hawaii but none of these proclamations provide a long-term solution to Hawaii’s and especially Maui’s housing affordability.

More on MLP’s Management

Steve Case

Steve Case, (AOL Co-Founder) is a MLP board member and is MLP's largest shareholder. Case owns 62% of the company. Steve has also founded a company called Revolution LLC. The building arm of Revolution LLC, Revolution Places has developed other plots of land into extravagant resorts. Revolution Places has just finished a new Waldorf Astoria hotel in Costa Rica. This 190-room hotel comes complete with luxury branded residences called Waldorf Astoria Guanacaste and in many ways is similar to MLP’s Kapalua resort. The Waldorf Astoria is currently booking reservations for May 5th and later and is the latest example of Steve Case’s successful building projects.

Glyn Aeppel

Glyn Aeppel was appointed to MLP's Board of Directors in July of 2022 and has extensive experience in the luxury hotel industry. Founder and CEO of Glencove Capital, Glyn Aeppel has over 35 years of experience developing hotel brands and "has sourced, closed, and financed real estate investments of well over $3 billion" in both the United States and Europe. She also serves on the board of Simon Property Group.

John Sabin

Long time CFO for two of Steve Case's companies Revolution LLC and Case Foundation, John Sabin is always close by Steve's property development endeavors. John was also appointed to MLP's Board of Directors in July of 2022.

Scot Sellers

Mr. Sellers sits on the boards of some of the most prominent building companies in the United States including most recently joining the board of Howard Hughes, taking Bill Ackman’s seat. He joined MLP’s board in March of 2023. Scot used to be the CEO of Archstone, one of the largest multi-family housing companies in the world. He was CEO for almost 20 years where he grew it from several hundred million dollars in assets to a total capitalization exceeding $22 billion.

Race Randle

In March of 2023 MLP named Race Randle as the company’s new CEO. Randle has an impressive resume of accomplishments including a redesign on Ward Village in Honolulu that involved building 4,300 residential units on 60 acres of land. Ward Village has gone on to win an impressive plethora of accolades including “Master Planned Community of the Year” by The National Association of Home Builders, "LEED for Neighborhood Development Platinum certification" by the U.S. Green Building Council, and “Best-Planned Community in the United States” by Architectural Digest.

Ken Ota

Ken Ota joined MLP’s board as an independent director in January of 2024. Mr. Ota founded the Pacific Pipe Company as President and CEO. This plays into MLP's business strategy as the company owns several potable water wells, non-potable irrigation water ditches, reservoirs, and transmission systems that provide sales of potable and non-potable water in West and Upcountry Maui. Ken is also currently on the State of Hawaii’s Licensing Board of Engineers, Architects, Surveyors, and Landscape Architects. This is possibly the most important piece of Ota's qualifications to work with MLP. Without approval from these boards MLP can't build anything.

Catherine Ngo

Also joining MLP as an independent director this past January was Catherine Ngo. Ngo was an Executive Vice Chair person and is now serving as Chair of the Central Pacific Financial Corp (NYSE:CPF), a Hawaiian bank based in Honolulu. For six years prior to that Ngo served as the President and CEO of Central Pacific Bank. A University of Virginia School of Law graduate Ngo spent seven years practicing private law before becoming the Executive Vice President of Silicon Valley Bank until 2005 when she helped found Startup Capital Ventures as a general partner. Ngo also serves as a board member for Hawaii Gas, chairs the Federal Reserve Bank Community Depository Institutions Advisory Council for the 12th District, and is a member of the National FRB CDIAC in Washington, D.C. All of this experience around banking and financing could prove crucial to the company’s ability to properly finance both its current and future land development ventures.

All of MLP’s management appears to be top notch and well suited to handle the difficulties that may arise when attempting to build anything in the state of Hawaii. This is a large reason why I believe that MLP has a decisive edge over Maui’s other large land owners like Kaanapali Land, LLC (OTC:KANP) which have a lot of valuable land at their disposal but are not as far along with their entitlements and don’t have a management team with as impressive of a resume when it comes to large scale building projects.

Conclusion

I hold MLP in my portfolio currently and while I have already made some handsome gains on the stock myself, I would still purchase shares of MLP today. As MLP begins to develop its properties, most likely through selling off its parcels to builders including Revolution Places LLC, and the profits that the company makes from these land sales begins to roll in, investors will likely start to catch wind of these developments and buy into the stock. The reason I am so bullish on MLP is because they not only have a mountain of value waiting to be discovered but that they also have a management team that has, over the past two years, been assembled to create the perfect pool of talent for the company to realize this value.

Disclosure: I am long Maui Land & Pineapple Company, Inc. (NYSE:MLP) and will buy or sell my shares anytime following this article. This is not financial advice. I am not a financial advisor. Do your own research.

This has been mispriced forever