Tiny Ltd: A Collection of Lousy Internet Companies

I don’t often look at companies to short. It is a tough game. You can be absolutely right on your analysis. The said company could be a complete fraud. Burning cash like crazy. A melting ice cube sitting in the Arizona sun. Despite all that, if you don’t get the timing right on a short you can lose significant capital.

I have had enough problems investing value stocks. So there have only been a few times in my career when I look at a company through the eyes of a short seller. This is one of those times. Though I am not currently short. I did want to pen my thoughts down on a company that appears to be operating on the brink of self-destruction.

Before we get into the financial details, we should back the story up for just a minute

The company in question has been touted as the Berkshire Hathaway of the internet. The two founders and co-CEOs, the next Warren Buffett and Charlie Munger. However, if you can read financial statements, you might come to a similar conclusion as myself.

All is not going well in the land of lousy internet companies.

I am always skeptical of anyone in the capital markets who is attempting to build the next Berkshire Hathaway. There is a graveyard of failed “Berkshires”. Men with egos so big they envision their future as the Omaha of whatever. Which is lesson one: never trust anyone who is attempting to build the next Berkshire.

Although I’d love to continue to rip on Ivy Leaguers who dance around mental models and Charlie Munger quotes, I think my time is better spent to discuss Tiny Ltd. (TINY.V) a Canadian micro-cap stock with a market cap of $336 million and enterprise value of $426 million. It should be noted that all figures will be in CAD unless otherwise noted.

Founded by serial Twitter poster, Andrew Wilkinson, Tiny was designed to become the Berkshire Hathaway of the internet. Through multiple bad acquisitions, a poorly designed IPO, a former CEO who is distracted by the attention of podcasts, Twitter, book tours, and now a balance sheet in rough shape, I believe that Tiny is a short and the most likely scenario is the equity value gets wiped out through bankruptcy or massive dilution.

Since 2016 the company has acquired 35 business. And according to their website they claim these are “wonderful” businesses.

I have spent a significant amount of time trying to analyze this company and I still can’t figure out what all of these acquisitions do or how they complement the company. I also cannot figure out what makes these wonderful businesses. The EBITDA margins are in the single digits and hardly any of the EBITDA drops to free cash flow. And to make matters worse there isn’t any tangible assets AT ALL. All of the “pretend” book value is made up of goodwill and other intangibles.

But that is not all. There are a variety of red flags in the financials that I will lay out point by point in this research report.

The first point is the fake EBITDA.

Fake EBITDA

What really puts me off about Tiny and makes me think that other retail investors are unaware of the dire financial situation is the misrepresentation of the company’s profitability. In the 2023 shareholder letter, which I urge everyone to read, you can find a lot of inconsistencies to what is really going on with the company.

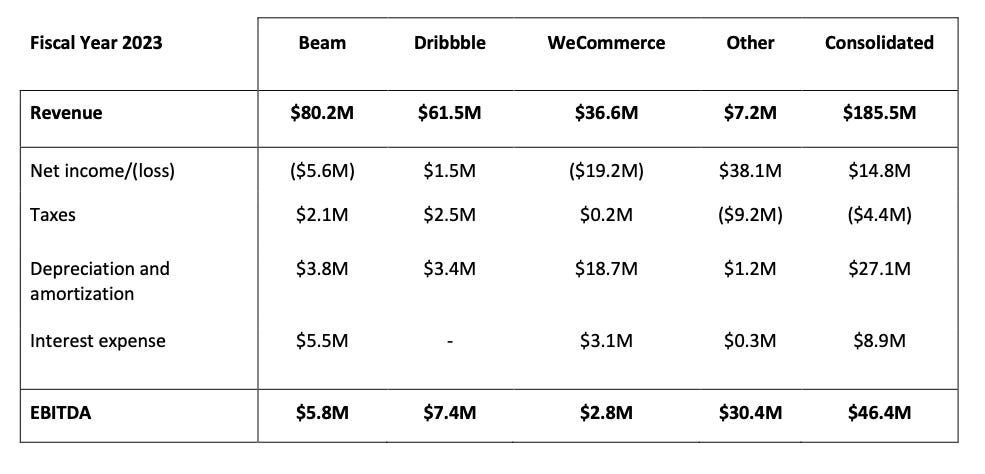

The first to note is the $46.4 million of EBITDA for 2023 seen below.

If you dig into this EBITDA, almost all of it is fake. A non-cash, one-time accounting trick that inflates the “earnings” portion of the formula.

Here is how the management team calculates EBITDA per their 2023 annual letter

Straight forward, directly from IFRS net income of $14.8 million. If you dig into how net income is calculated, per the 2023 annual report, you can see a gain on step acquisition of $42.8 million. This is a non-cash accounting trick that inflates net income by $42.8 million. Read this article to understand the accounting for a gain on step acquisition if you are new to IFRS accounting.

Not only is it non-cash, but it is one-time and non-recurring. They also add back an $8.7 million gain on write-down of contingent liability that will not be recurring along with a number of other items. Although, to Tiny’s credit, they did keep in the negative $13.6 million impairment within their EBITDA.

If you back out of the gain on step acquisition and the gain on write-down of contingent liability, and all else being equal, the EBITDA in 2023 was a shocking negative $5.1 million.

What irks me about this EBITDA number is a couple of points. First, Tiny highlights the $46.9 million of EBITDA in their 2023 presentation, right on the front slide.

Secondly, in the 2023 annual letter, Andrew drops a Charlie Munger quote saying that EBITDA is “bullshit earnings”. And then he proceeds to say they will eliminate the use of EBITDA in the 2024 investor documents.

My take is that Andrew Wilkinson knows that Tiny’s 2023 EBITDA of $46.4 million is all generated from a one-time non-cash accounting trick. Which means that 2024 adjusted EBITDA will be a fraction of the 2023 EBITDA. So why not throw in the silly Charlie Munger quote about how all EBITDA is bullshit, despite the fact you highlighted this on the front page of your investor deck for all investors to see.

And if you are still skeptical that the EBITDA is actually real, just take a look at the cash flow statement. Cash never lies.

For 2023, Tiny generated $3.4 million of cash from operations. A far cry from the $46.9 million of EBITDA. Profitability is unheard of in the tiny little Vancouver office.

I created a table for the adjusted EBITDA in the first six months of 2024 seen below. As shown, the adjusted EBITDA of only $13.4 million is a drastic drop from the 2023 adjusted EBITDA. And a lot of this adjusted EBITDA is generated from $6 million of interest expense, which is a real expense to the equity holders of Tiny.

Management

The management team of Tiny was formerly lead by Andrew Wilkinson and Chris Sparling. However, both of them stepped down as Co-CEOs on June 6th, 2024, as highlighted in this nonsensical Tweet. This is a major red flag. The Co-CEOs jump ship the year adjusted EBITDA will take a drastic step down. Not only that, but the stock is down 90% since going public and results are getting much worse. What happened to building the Berkshire of the internet? This is not a Buffett and Munger move in my opinion.

The new executives are Jordan Taub, CEO and Mike McKenna, CFO. Jordan was the CEO of WeCommerce, a company that Andrew purchased and subsequently took public (stock tanked from terrible results) which he then IPOed into Tiny. Prior to WeCommerce, Jordan worked at Constellation Software. Mike McKenna was the CFO of Lifespark, a company that appears to be on the verge of bankruptcy, from poor financial management.

I urge all readers to listen to the recent earnings transcript of Tiny where Jordan and Mike spoke for the first time to investors. It was one of the worst earnings calls I have ever heard. Jordan said “you know” 86 times and “umm” at least 100 times. This might be a Canadian Venture company, but at least hire executives who know how to speak to their investors.

Another issue I have is all of the related party transactions. Andrew Wilkinson has received fees through consulting services through a company he controls. Chris Sparling has received the same fees. Even director, Shane Parrish received fees (likely from his podcast).

And then there are just the weird things Wilkinson does.

Like charging people $10,000 per hour to speak with him.

Or how he called Tai Lopez a fraud back in 2020, but seems to be running a similar online guru persona.

And then Wilkinson got a divorce. This is not only a personal distraction from running a multi-platform business, but he has filed multiple Sedar filings showing he will or is dumping stock in the open market.

Then there is the book he wrote and the endless podcasts he does. I feel like all of these are distractions to running a public entity. And I am still unsure how he calculates that he is a billionaire when the equity value of $TINY.V is $336 million CAD. But that is just the Buffett disciple selling a book while his stock becomes a penny stock.

What is the most interesting event was the cash out refinance Beam LLC executed on May 20, 2022. On this date Beam drew $44.57 million on the revolver and another $5.7 million and declared a dividend of $50 million to shareholders. $12.3 million went to Tiny and $37.6 million went to related parties. This was a financial transaction that allowed insiders to lever Tiny up with debt and let them cash out millions for themselves.

This reminds me of when Warren and Charlie resigned barely a year after Berkshire went public, right after they saddled it with crippling debt…

The wheels appear to be coming off.

Valuation

I valued Tiny using a sum-of-the-parts analysis.

I valued Beam, Dribble and WeCommerce on an 8.0x EBITDA multiple using 2023 EBITDA figures. It should be noted that EBITDA across all business lines are down significantly since 2023. I placed a zero EBITDA figure on the “other” business line as it appears that is where the non-step accounting charge was running through. I would also like to point out placing and 8.0x EBITDA multiple on these businesses is generous at best. These are not tech companies. These are a collection of low single digit EBITDA margin service type businesses. They likely deserve a 3.0-4.0x multiple.

I also placed a $50 million value on the Tiny Fund. Tiny Fund commenced operations in August 2020 and has $150 million of committed capital. Tiny LTD is a 20.24% LP in Tiny Fund and receives 30% carry above 8% hurdle. Tiny LTD has invested $29.95 million into Tiny Fund I out of a total $148 million total fund size, resulting in Tiny Ltd. LP having 20% interest. The Fund went from $150 million to $148 million from a few LPs reducing commitments. The holdings of the fund include the following:

AeroPress (93.76%)

Letterboxd (60%)

Abstract (70%)

Conference Badge (95.8%)

Girlboss (75%)

BeFunky (84.96%)

MediaMap (57.9%)

WholesalePet

Mateina (50.01%

Other minority positions

My guess is that Tiny Fund acquired most of these positions at the peak of the VC bubble in 2020/2021 when interest rates were at 0% and valuations at the peak. Placing a value of $50 million on the fund assumes they make close to a double on their invested capital. The recent capital draws suggest otherwise.

Finally, the proper way to run a sum-of-the-parts analysis is to include corporate costs. Tiny doesn’t have a traditional line item for SG&A but I think it would be the $2.8 million of “professional fees” in the income statement in the most recent quarter. If we annualize this number we get an annual corporate expense of $11.2 million. Assuming it only takes 12 months to sell the entire company, this $11.2 million of corporate expense would take the sum-of-the-parts valuation down to $0.37 per share.

Debt: The Final Dagger

The final item that should be noted is the debt that Tiny Ltd. has on their balance sheet. Per the recent quarter, Tiny has $121 million of debt. This includes $40 million on a term loan and $80.4 million on a revolver. What is interesting about debt is the recent amendment.

On June 28th, 2024, Tiny entered into an amended agreement to amend its loan covenants on their revolver with National Bank of Canada. The following was removed:

Minimum liquidity above $6 million

And Monthly EBITDA of $10 million

In return for these amendments Tiny needs to de-lever their balance sheet significantly. Here are the new terms

Total amount available on the facility is $70 million to September 30th, 2024

$67 million between October 1, 2024 and December 31, 2024

$64 million between January 1, 2025 to March 31, 2025

$61 million between April 1, 2025 to June 30th, 2025

$58 million July 1, 2025 and thereafter.

As of the quarterly report Tiny had $68.5 million borrowed on the revolver. The company will need to pay down debt by $20 million by July 1, 2025. Given the company hardly generates free cash flow, and it appears that the businesses are not doing well, the company will likely drain their $22 million cash balance to pay this debt down. Or they will continue to raise equity and dilute shareholders like they did on June 4th, 2024. It is also interesting to note that the company was forced to amend their revolver to get rid of the minimum EBITDA, because their EBITDA is all gone!

Conclusion

Tiny Ltd. has issues. It is a Canadian venture stock with hardly any cash flow. The 2023 EBITDA had a one-time step on acquisition accounting gain. The Co-CEOs have stepped down. And the face of the company is forced to sell shares because of a divorce. With an over-levered balance sheet and declining profitability, I see substantial downside for equity holders. I don’t see how Tiny Ltd. can get itself out of their debt without fire selling assets or raising equity. My price target is $0.44 per share.

Disclosure: I am not short Tiny Ltd. (TINY.V). This is not financial advice. Do your own research

Stock collapsing after that miserable Q3 report. Slow motion train wreck. The will run out of cash early next year.

Great analysis, very interesting. One thing to consider would be the talent pool below the former co-CEOs and the new CEO, CFO tandem. I am not contesting your analysis at all, but often there is a lot of talent just below the top of an organization, and I would not be surprised if that was the case here as well. Looks like a screaming short. Looking forward to reading more of your stuff.