Dollar General Shares Currently Priced at a 10 Year Low

Stupid Simple, Likely Profitable.

The Pitch

Dollar General (NYSE: DG 0.00%↑ ) is currently trading at its lowest share price in the past decade. DG’s share price had risen sharply to exuberant highs both during and post COVID. Once their margins began to slip however, Dollar General’s stock fell erratically, past what I would consider to be reasonable. If DG can bring their EBIT margins back up to 9.0% (where they were pre-COVID) and maintain their capital expenditures at a rate close to what they’re at now (3.6% of revenues), then I believe the company’s stock could be worth $108 per share.

Dollar General has experienced sales growth every single year since 1990 except for 2021, due to the effects of the COVID-19 Pandemic. Right now the company’s net and EBIT incomes are similar to the company’s 2016 - 2017 net and EBIT income figures. This is despite DG experiencing growth in their gross profit every year as well as the company’s revenues nearly doubling since that time period. The company is working to improve their profitability by focusing on inventory reductions which should then improve shrink rates and inventory damage. This should also decrease inventory transportation costs through increases in shipping efficiencies. Having a reduced inventory will also help to decrease the need to mark down inventory, which has in recent years, done some serious damage to DG’s margins.

Progress on Cost Cutting Efforts

DG has been seeing their inventory shrink reduce throughout 2024 after spiking in 2023. The company has also been reducing their transportation costs. They still need to get a handle on inventory damage and mark ups but, by DG continuing to reduce their inventory, the company’s remaining inventory should become more easily manageable. This would not only help to reduce inventory damage, but would also help the company keep a more accurate inventory of what and how many products they have in stock. This will help Dollar General make decisions more quickly about what products need to be ordered and what products aren’t selling which should in turn help to reduce DG’s mark downs.

Slowing Down New Store Openings

While Dollar General has based its business model off of constantly expanding by opening up new stores, the company really ramped up the pace of these new store openings over the last five years. Now that Dollar General is focused on retaining margins they have slowed down the pace of new store openings. During 2021, DG opened 1,050 new stores and remodeled or relocated 1,852 stores, in 2022 they opened 1,039 new stores and remodeled or relocated 1,922 stores, in 2023 they opened a total of 987 new stores and remodeled 2,007 stores. In fiscal 2024 DG plans to open 730 new stores and remodel approximately 1,620 stores.

A focus on reworking their current stores and slowing down the pace of their new store expansions will, I believe, help DG continue to reduce shrink, lower transportation costs, and finally get a hold on their inventory damage problem. DG also has $250 million less in bond maturity payments due in 2025 as compared to 2024. This lower bond maturity payment combined with Dollar General’s efficiency improvement efforts if executed correctly, should help the company turn their business performance around and help to instill confidence back into investors.

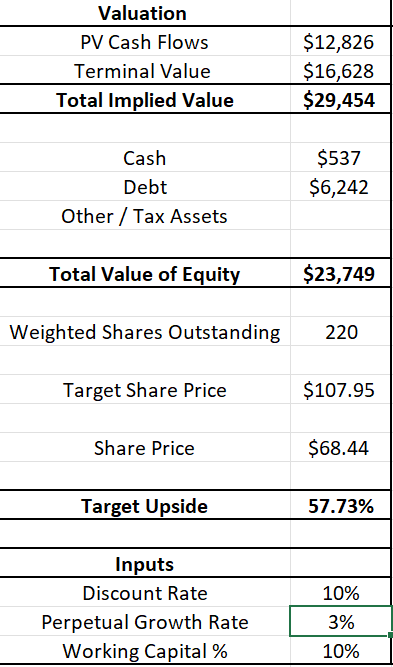

A Discounted Cash Flow on Dollar General

I ran a discounted cash flow analysis on Dollar General to see what their stock would be worth should the company be able to raise their EBIT margins. If DG can bring their EBIT margins back up to 9.0% over the course of the next three years, then maintain that EBIT margin through 2035 while keeping their capital expenditures at 3.6% of their revenues, the company’s stock should see a substantial increase in share price.

If DG is able to bring their margins back up over the course of the next couple of years their cash flows values should be worth $107.95 per share. If they are only able to bring their EBIT margins back up to 8.0% then DG’s cash flow values still appear to be worth over $90.00 per share.

My Conclusion on Dollar General

My Dollar General thesis is caveman simple. DG has seen its margins erode. The company is attempting to correct this through better inventory control. If they succeed the stock should see a substantial price increase as investors have been overly harsh towards discount stores and dollar stores in general. Any good news regarding sustainable developments concerning DG’s operations will likely change investors’ tune about the stock and this overly bearish investor sentiment may turn into an overly bullish sentiment. That’s when you cash in. Stupid simple, likely profitable, that’s my Dollar General pitch.

Disclosure: I am long Dollar General ( NYSE: DG 0.00%↑ ) and will buy or sell my shares anytime following this article. This is not financial advice. I am not a financial advisor. Do your own research.

The remodelling and Project Elevate remodelling offer better returns than the newly opened stores.

Good progress on Back to Basics plans and might start to see that in income statement soon. If op margins can get back to 5% that could be 2b in op income, which isn't too bad at these prices.

Their consumers are struggling though based off the survey that they shared in Q2 results

Thanks Jack very interesting