My Research Process, From Whiteboard to Write-up

A how-to for finding, analyzing, and underwriting a stock — using my actual workflow.

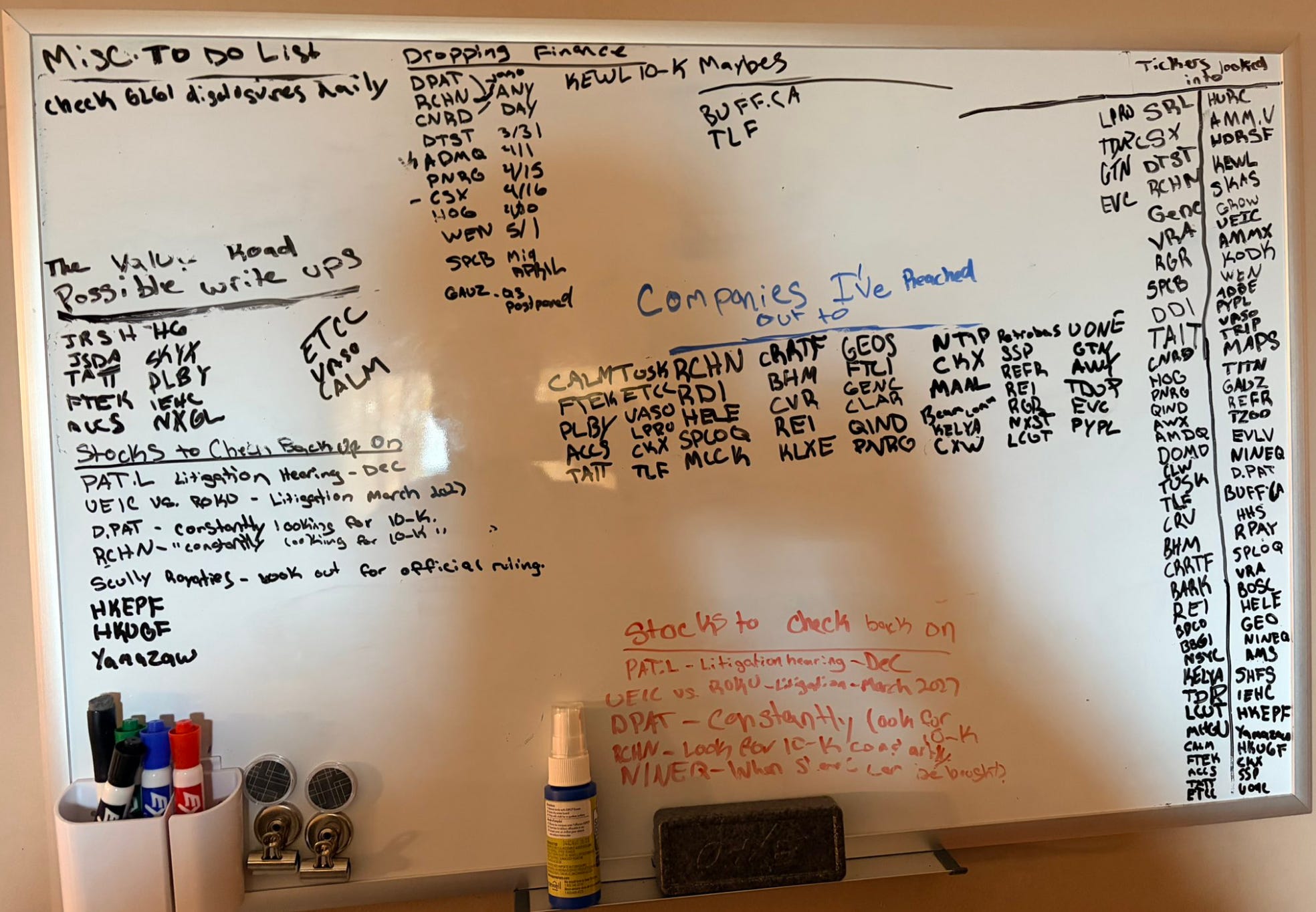

This is the whiteboard in my office. It looks chaotic, and that’s because it is. Four marker colors, a “Companies I’ve Reached Out To” grid that takes up half the surface, a list of tickers I’ve looked into that runs eighty deep, and a “Stocks to Check Back On” section I cared about enough to write twice — once in black, once in red.

People sometimes ask me what my “process” is. The honest answer is: it’s whatever ends up on that board. But there is a process underneath it, and the board is just where it gets externalized so I don’t lose track. Here’s how it actually works, step by step, in the order an idea moves through my brain.

Step 1: Sourcing — read the people who are already doing the work

I don’t run screeners. I used to, and I might again, but the truth is the best ideas I’ve ever worked on came from other investors — Substack write-ups, Twitter/X threads, VIC posts, fund letters, the occasional message board if I’m being honest. The reason isn’t that I’m lazy; it’s that a screener gives you a ticker and a multiple, but another investor gives you the question they’re trying to answer. That question is the actual idea.

What I’m looking for when I read:

A ticker I’ve never heard of, or one I’d written off.

A specific catalyst or anomaly the writer is pointing at — not “it’s cheap,” but “it’s cheap because the market is missing X.”

A name that’s small enough that I have a realistic shot at knowing more than the marginal holder. If it’s a $40B mid-cap, I close the tab.

When something hits, it goes onto the far-right column of the board: “Tickers I’ve Looked Into.” That column has no commitment attached to it — it’s just a holding pen. The point of writing it down isn’t to remember the thesis; it’s to remember that I’ve already had the conversation with myself, so when the ticker shows up again three months later I don’t start from zero.

The funnel from here is brutal and that’s by design. Of the ~eighty names in that column, maybe half ever get a second look.

Step 2: First-pass triage — kill it fast or move it forward

Before I do any real work, I want to know if the idea is dead on arrival. I’m trying to disqualify, not qualify. The fastest way to lose a month is to fall in love with a thesis before stress-testing the obvious.

The triage questions I run, in this order:

Is the balance sheet going to kill me? Quick look at net debt, maturities, and whether the equity is real or a residual after the bondholders eat. If there’s a refinancing wall in the next 18 months I want to know now.

Is the business actually a business? Revenue trend over five years, gross margin stability, whether the cash flow statement and the income statement tell the same story. Companies whose “earnings” never become cash are not companies, they’re stories.

Who owns it and who’s running it? Insider ownership, recent insider buying/selling, and whether the CEO is a builder, a steward, or a guy who’s about to dilute me.

What’s the actual catalyst? “It’s undervalued” is not a catalyst. A 10-K dropping, a litigation ruling, a spin-off, an asset sale, an activist filing, a forced seller unwinding — those are catalysts.

If it survives triage, two things happen. First, it earns a spot in the middle column: “Companies I’ve Reached Out To.”Second, if there’s a catalyst on a knowable timeline, it goes on the “Stocks to Check Back On” list with the date.

About that calendar discipline — the “Dropping Finance” column on my board is just a list of filings I’m waiting on with their drop dates. DPAT, RCHN, CSX on 4/16, HOG on 4/30, and so on. The reason I write the date down is simple: half of micro-cap edge is being there when the filing drops. If you’re refreshing EDGAR an hour after everyone else, you’ve already lost.

Step 3: Reach out to IR — the cheapest edge nobody uses

This is the step most retail investors skip and most professionals take for granted, and it’s where I think the biggest free lunch in micro-cap investing still lives.

I email investor relations. I ask to schedule a call. Sometimes I just ask three specific questions over email. The hit rate is terrible — maybe one in three writes back, maybe one in five gives me anything useful, maybe one in ten produces a genuine insight. But the insight, when it comes, is enormous, because the marginal holder of a $50M company has never spoken to the CFO. You have.

Three rules I follow when I reach out:

Be specific. “Tell me about the business” is what an analyst with no edge asks. “On page 47 of the 10-K, you booked a $2.3M impairment against the segment you’re now guiding to grow — can you walk me through the timing?” is what someone they want to talk to asks.

Read everything first. Every 10-K, every 10-Q, every proxy, every transcript. If you ask IR a question whose answer is on page 12 of the latest Q, they will (correctly) write you off as not serious.

Track who you talked to. That entire middle column on my board is people I’ve reached out to. It’s there because three months later I will absolutely forget whether I ever spoke to GEOS’s CFO, and rebuilding that context from scratch is a tax I refuse to pay.

The phone call is where the thesis either gets real or dies quietly. Both outcomes are good. The bad outcome is no call at all.

Step 4: Deep underwriting — the four lenses

For names that survive triage and IR contact, I do real work. My underwriting runs on four parallel tracks, and I deliberately do them in different sessions so I don’t bias one with the conclusions of another.

Lens 1: Reverse-engineer the financials. I don’t just read the 10-K — I rebuild it. Pull the last five years of segment data into a spreadsheet, normalize for one-time items, separate maintenance capex from growth capex, recalculate working capital changes. The goal is to get to a number — owner earnings, free cash flow, normalized EBIT, whatever the business calls for — that I trust because I built it. The reported numbers are a starting point, not an answer.

Lens 2: Primary research and IR. Covered above. This is where qualitative texture comes in — management quality, customer concentration risk, competitive dynamics, what’s actually happening on the ground that the filings can’t or won’t tell you.

Lens 3: Asset value / sum-of-parts. For a lot of the names I work on, the earnings story is secondary. What I really want to know is: if this company were liquidated tomorrow, what would the parts be worth? Real estate at market, not book. Inventory at recovery value. Marketable securities at quote. Operating segments at comp multiples. NOLs at a reasonable discount. This is where the names with .L, .V, .CA, and pink-sheet suffixes earn their keep — the asset value is often shockingly disconnected from the quote.

Lens 4: Catalyst and legal docket tracking. If the thesis depends on something happening — a court ruling, a filing, a transaction — I track it explicitly. PAT.L has a litigation hearing in December. UEIC vs. ROKU resolves in March 2027. Scully Royalties is waiting on an official ruling. These are on my board because they’re the things that will actually move the stock, and the world will not remind me when the date is approaching. PACER, courtlistener, SEC full-text search, and the company’s IR calendar are all part of this. If the catalyst slips, the thesis often slips with it, and I’d rather know that on day one than month nine.

When all four lenses agree, I have a thesis. When three of four agree, I have a question. When two of four agree, I move on.

Step 5: The buy decision

Surviving all four lenses gets a name onto the shortlist. It does not get it into the portfolio. Plenty of stocks are good ideas in the abstract and bad ideas at today’s price, in today’s size, against what I already own. The buy decision is its own step, and I keep it separate on purpose so I don’t confuse “this is a great business” with “I should be long this tomorrow.”

Before I size a position, the name has to clear four gates:

Can I state the thesis in one sentence, the catalyst in one sentence, and what would make me wrong in one sentence? If I can’t, the work isn’t done. Vague theses become losing positions because you can’t tell when you’re wrong — you just slowly stop talking about them.

Is the price actually right right now? A name can be a great business and a bad buy. I want a clear gap between my underwritten value and the quote — enough margin that I’m paid for being wrong on parts of the thesis, and enough that I’m not buying at a level where the catalyst is already priced in.

Does it fit the portfolio I already have? If I already own three names with the same catalyst (delinquent filer becoming current), or three names exposed to the same underlying risk (small-cap energy, distressed Canadian listings, whatever), a fourth doesn’t diversify me — it concentrates me. I’d rather pass on a good idea than double-stack a risk I’m already paid to take once.

What’s the path to exit? I want to know how this position ends before I open it. Catalyst hits and stock re-rates → trim or exit. Catalyst slips past a defined date → reassess or exit. Asset value gets harvested → exit on the harvest. If I can’t sketch the exit on day one, I’m not really underwriting; I’m hoping.

Sizing comes out of those answers, not out of conviction in isolation. A high-conviction name with a binary catalyst gets sized smaller than a moderate-conviction name with hard asset coverage, because the loss profile matters more than the upside narrative. The position size is the risk decision.

Once a name clears all four gates, it stops being research and starts being a position — which means the work shifts from underwriting to maintenance.

Step 6: Maintenance — the part nobody talks about

The board has a section called “Stocks to Check Back On.” It’s the most boring part of the whole process and probably the most important. Owning a position is not the end of the work; it’s where a different kind of work begins.

What I maintain:

Filing calendars for every position, so the 10-K is read the day it drops.

Catalyst dates for anything thesis-relevant — court hearings, settlement deadlines, lock-up expirations, special meeting votes.

A “constantly looking for 10-K” list for delinquent filers. (RCHN and DPAT live here. They’re delinquent for reasons that matter to the thesis, and the filing is the catalyst.)

A re-check trigger on dormant ideas. If a name I passed on six months ago has dropped 30%, or the catalyst I was waiting on has hit, I want to know.

This maintenance layer is why the board exists at all. The brain is a leaky bucket; the whiteboard is a backup drive.

The whole funnel, in one paragraph

Read what other smart people are working on. Write down every ticker that survives a glance. Triage hard and fast on balance sheet, business quality, ownership, and catalyst. For survivors, email IR and ask better questions than the marginal holder is asking. Then underwrite in four parallel passes — rebuild the financials yourself, talk to people, value the assets independent of earnings, and track the catalyst on a calendar. Buy only the names where the thesis, catalyst, and disconfirmation each fit in a sentence, the price gives you margin, the position fits the book you already own, and you can sketch the exit on day one. Maintain everything else. Externalize all of it onto a surface bigger than your skull, because the skull will fail you.

That’s the process. The board is just where you can see it.

If you want to see which names from the whiteboard actually make it into the portfolio — and which ones get killed at the buy gate — that’s what this newsletter is for. Subscribe, and you’ll find out which side of the funnel they end up on.

as always real helpful quality stuff. thanks.

Well written explanation- Thankyou