My Best and Worst Investments Ideas and What I Learned From Each of Them: Part 1

Knowing When You Are Wrong

Why I Write About Stocks

Before starting The Value Road, I was writing pretty consistently for Seeking Alpha. I began writing about stocks not because I wanted to give people financial advice but because I wanted to be able to organize and flesh out my thoughts to a greater extent than merely thinking quietly about these things allowed me to do. I also began writing because I wanted an objective record of what I thought a good investment was, before pulling the trigger on buying into a company. If I record my thoughts I can’t “remember things differently” a year or more later if my investment thesis was to go south. I now have the ability to go back to my original thoughts and see if my idea just failed to play out or, if I missed some piece to my investment thesis that was crucial to understanding the company under the microscope.

Beyond using financial writing as a way to keep myself honest about my investing decisions, writing for Seeking Alpha exposed me to criticism about my investment philosophies and ideas. While nobody usually enjoys their work being criticized I actually welcomed the discussions. Seeing things from the perspective of other investors helped me look at investing from different angles. While I may not have agreed with all of the criticism, I looked into each bit of criticism with an earnest curiosity and tried to see every argument from the opposition’s point of view. Then I let time tell who was right.

Gaining Success Through Value Investing

I began to beat the market through the value investment philosophies I write about here. I didn’t just beat the market, but I beat the market consistently. Three years ago I switched from investing mindlessly into a bunch of CNBC stock picks and began investing in smaller capitalized companies with a lot of assets and little to no debt. This will be my third year beating the market. I used to trade with TD Ameritrade but now trade through Charles Schwab. This is because Schwab bought out TD Ameritrade’s brokerage accounts. Unfortunately I am unable ( or unaware of) how to access my TD Ameritrade non realized gains history but here’s my Charles Schwab returns vs the S&P 500. As you can see, my return information since available beats the composite returns by a minimum of 10.0% and my year to date returns by 12.0%.

When Investments Do Not Work Out

While I have been making some good calls on my brokerage account and on my Seeking Alpha picks, I have made some poor decisions in the past as well. If you have the courage to honestly assess yourself and what you did wrong in that moment, these bad decisions can be turned into important life lessons. I personally feel like I have learned a mountain more about value investing from my mistakes than I did from my successes. I have a fairly large conviction that value investing works and when I make a lot of money and beat the major indexes I am not surprised. When I lose money or an investment underperforms, I treat it as a learning opportunity.

RCI Hospitality Holdings

I invested in RCI Hospitality Holdings, Inc. (NASDAQ:RICK). This is an adult nightclub company. Their main business model is actually fairly solid. Cities do not enjoy new strip clubs going up and try and discourage this through zoning or ordinances. This helps the existing strip clubs that do exist operate without much competition. The people that own most of the existing strip clubs in the US are getting old and aging out of the business and with no new blood coming in to take over these companies, when the time comes to sell, these clubs sell for cheap. RCI would then come in and buy up these clubs at discount value and continue to absorb the cash flow these establishments generate.

All of this sounds like a sure-fire to generate free cash flow but the management team at RCI has bigger prospects for the company. They had been intent on expanding a rather unprofitable sports bar business called Bombshells. They had also been trying to open up casinos in Colorado. At the time I had accepted the bombshells expansion as a failed business that RCI would probably keep limping along with but not something that would be a deal breaker. I had high hopes that RCI would get its casino businesses opened and could begin to generate cash flow from that. RCI was also working on a subscription based website similar to OnlyFans, in an attempt to generate new sources of revenue.

If RCI was able to get their Central City casino projects off of the ground, investors would have probably begun to pour in. Instead these projects were met with endless delays. Now it appears that they are selling off these properties as they have apparently given up trying to get the permits and approvals necessary to operate a casino. While these projects were being delayed, RCI was bleeding money investing into the properties. Not only that, the management couldn’t focus on running their core business, strip clubs. Not that they seemed intently focused on getting their casinos up and going or turning around Bombshells either. CEO Rick Eric Langan seems to spend a lot of time drinking at clubs and going to high profile events while their businesses did this…

“During fiscal 2024, Bombshells sales mix was 54.3% alcoholic beverages and 45.7% food, merchandise, and other. Segment gross margin (revenues less cost of goods sold, divided by revenues) was approximately 75.9%. Bombshells segment revenue decreased by 9.2%, while income from operations decreased by 263.7% from prior year. Same-stores sales for Bombshells in 2024 was -18.4%.” - RICK’s 2024 10-K

“Looking at our list of new projects, we have opened, converted, or enhanced seven locations to date this fiscal year, and we are working on opening, reopening, or reformatting seven more as fast and efficiently as possible. As per this effort, we formally withdrew our application for Colorado casino license to better focus on projects that will provide more immediate results.” - Eric Langan - CEO of RICK - RICK’s 2024 Q3 Earnings Call Transcript

This obviously has had catastrophic consequences for RCI’s income.

RCI’s CEO also seems to have an excuse for why his GAAP figures are so bad compared to his Non-GAAP figures.

“But total company sales declined due to a hurricane and a fire resulting in lower EPS. However, non-GAAP EPS, net cash provided by operating activities, and free cash flow, all increased.” - Eric Langan CEO of RICK - RICK’s 2024 Q4 Earnings Call Transcript

Reconsidering My Decision

The constant excuses and preference to non-GAAP figures to show progress because GAAP figures are constantly underwhelming made me back out of my position in the company. I had at that time stumbled upon a promising investment that I thought could more than make up for the losses I had incurred being invested in RCI. We’ll be talking about that investment in part two of this newsletter, where I will go over my best investment call I’ve made while writing about stocks.

With RCI I lost faith in the management team and their ability to stay within their lane of competency. My lesson from this is always pay close attention to who runs the company. This doesn’t just mean pay attention to what management says during press releases and earnings calls. If a member of management has a LinkedIn, Twitter, or other form of social media account, snoop around on it. Looking at what Eric Langan and others closely involved with the company had been up to began to make me uneasy about investing in RCI as their business aspirations appeared to be larger than their attention span. It was at this point that I began to seriously reconsider my investment and look for alternative market opportunities.

When To Call It Quits

I consider this a serious lesson learned. I lost something like 20.0% of the money I invested in RCI when I decided to sell. It might be hard to do but when reality continuously plays out in the opposite direction of your business thesis for a company, it is time to sell. Admitting you are wrong is a hard thing for a lot of people to do but it can save you money. It can also speed up the rate at which you learn from mistakes and save you a lot of heartache and financial loss.

The good thing about value investing is, if you invest in businesses with a lot of financial assets, these assets can be sold off when the company finds itself in trouble. This happens to be the case with RCI. As highlighted earlier in a quote referencing an earnings call from Q3 of this year, RCI abandoned its attempts to open up casinos in Colorado. In RCI’s 2024 Q4 earnings call, Eric talked about selling off this property to recoup some of these losses. This looks to have pleased investors and if I had held the stock at the price I recommended it at I would have actually made an 8.42% return but… I would have been way under the S&P 500 index return of 14.76% since that time period. This highlights the flexibility that companies have when they have a large asset base at their disposal. You can dig your company into a pretty deep hole and still walk up a pile of money funded by asset sales to get out of it. This seems to be what RCI is attempting to do now.

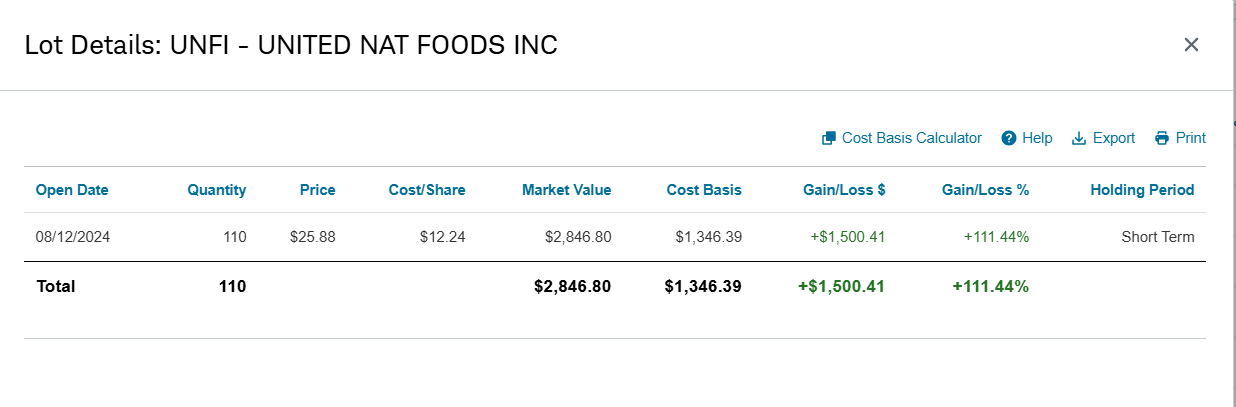

The stock I had invested in with my diminished RCI investment funds has given me a 111.44% return since I bought into it in August and will be the topic of part two of this newsletter. The company? United Natural Foods, Inc. (NYSE:UNFI)

Disclosure: I do not own shares of RCI Hospitality Holdings, Inc. (RICK). I am long United Natural Foods, Inc. (NYSE:UNFI) and may buy or sell my shares at any time following this article. This is not financial advice. I am not a financial advisor. Do your own research.

Its been 3 months writing on seeking alpha myself, really enjoying the journey 🙂

Outperforming in 2024 as a value investor is quite the achievement, congrats. Well done also for being willing to sell at a loss when there was something better to be had - not a psychologically easy thing to do.