A Cheap Stock for Expensive Fashion

New Boot Goofin'?

Today I’m going to be writing about a company with a $110 million market cap and an enterprise value of just $87 million. Looking in the rearview mirror to 2015, this company hasn’t had a net loss or operating loss except for 2020. This company sells its products to the military as well as to normal consumers and has recently been working to expand their military product lines towards the civilian market. This company also has a history of paying out special dividends when they sell off assets and has a purchase sales agreement for the sale of 168 acres of undeveloped land in Berkeley County, South Carolina for $1,760,000 on or before April 30, 2025. I’m currently waiting on a press release regarding that sale to drop any minute. If that sale goes through I believe a dividend could be in store for share holders.

This company is so far experiencing a slump in their earnings as compared to last year. This company has a long history of pulling through tough times though and it’s remained profitable while doing it. This slump we’re seeing in the company’s sales as people pull back on discretionary spending may provide a runway for generating some handsome returns in the future.

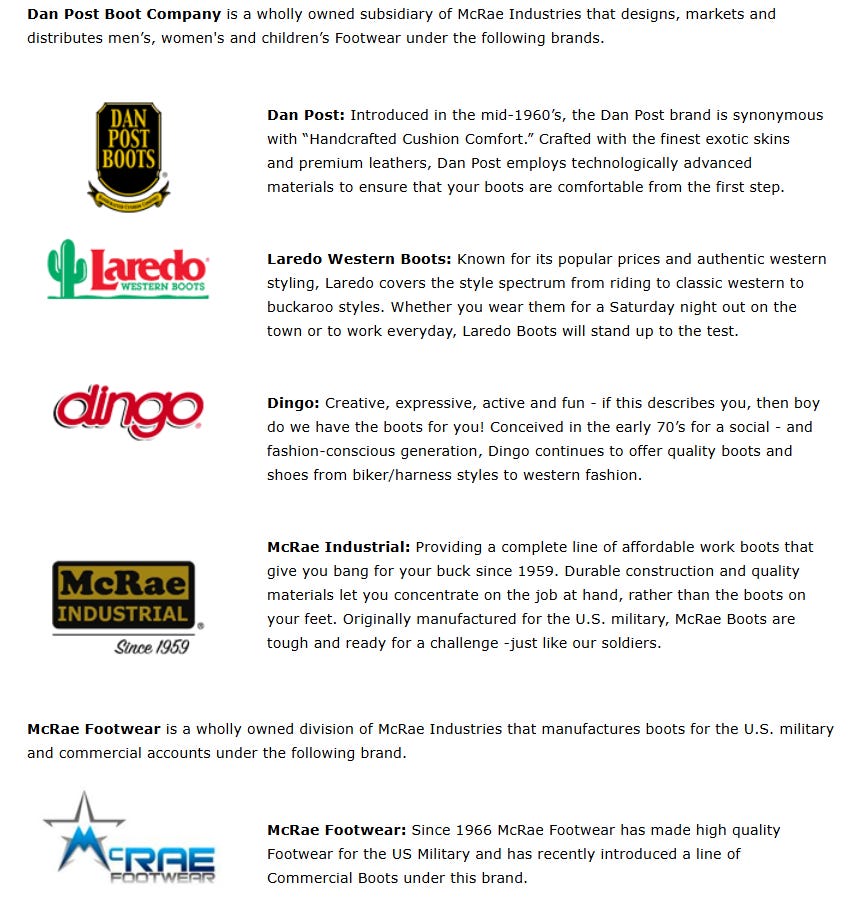

McRae Industries, Inc. has both Class A ($MCRAA) and Class B ($MCRAB) common stock outstanding. The company makes boots, more specifically work boots, western boots, and military boots. These products are branded McRae Industrial, McRae Footwear, Dan Post Boots, Laredo, and Dingo.

As I said earlier this company has a $110 million market cap and an enterprise value of just $87 million. This business looks cheap and I would normally consider McRae to be a potential buy based off of their cheap EV and relatively fair NAV figures combined with their long history of maintaining profitability. The factor that makes me strongly reconsider McRae as a company worth investing in is the fact that the company manufactures a lot of their products (mainly their entire western style boot catalog) in Mexico, India, and China. Here’s what Vice President James McRae had to say about that in a blog the company had wrote on their website.

“ “We were manufacturing our western boots at the two factories in Tennessee,” Jim says. “But all our competitors in the western boot market had gone offshore. We eventually followed suit and moved production of our western brands overseas – while continuing to manufacture our military boots in the North Carolina and Tennessee factories.” Today, Laredo and Dingo brands are made in China and India, and Dan Post is made in Mexico.”

- A Blog Entitled “Steps in a New Direction” posted on the company’s website.

Clothing and footwear manufacturers are going to be some of the hardest hit industries from the Trump administration’s tariffs and I am having a very hard time imagining a world where these new trade policies do not create a negative effect for McRae. On top of tariffs potentially eating into the company’s profits, they could also create supply chain disruptions.

I went to some TSC (Tractor Supply Company) stores around me to try and see the company’s products in person. When I got to TSC there was only two pair of boots on the shelf, both the same style of Dingo brand boots, both with significant mark downs for clearance. There was also no display for the boots anywhere in the shoe sections of these stores. They were located on a random shelf amongst other brands. While looking at the inventory of two TSC stores can’t be totally reflective of the company’s overall stocked supply across all of its retailers, it does trouble me a little bit to see McRae not have their products visible or stocked in the stores I went to. I don’t know if this is due to poor in-store sales or from McRae experiencing supply chain disruptions but, it does little to build my confidence that this is a brand I want to throw money at. It’s a shame too because their online presence looks rather sleek, especially for a company that makes “Rural” clothing.

Using China as a manufacturing hub while we have a 145% tariff on the country can’t be a catalyst for future business success. Nobody knows how long these tariffs will stay in place and that makes it impossible to predict with any certainty the future of a clothing or footwear manufacturer like McRae. For this reason I can not bring myself to buy shares in the company. At least not right now, even with the prospects of a potential special dividend looming.

Wrapping It Up

This is a company I will be keeping an eye on for possible future investment. Right now isn’t the time however to take a chance on a company who’s manufacturing is tied so closely to China. Any other time I would be much more likely to invest in McRae Industries. They’ve got an impressive record of profitability in an industry where that’s not (at least from what I’ve seen) usually the case. I’ve looked at a lot of companies that sell shoes or clothing and their business results year to year can often be much more volatile that McRae’s. I think this company has done a lot of things right over the years. Unfortunate as it is however, new global trade developments are still ongoing that have the potential to blow a huge hole in the clothing manufacturing industry and in my opinion it’s too early to tell which company is going to be able to pivot into a new age of global trade and who will fail under the new rules of this global trade game. I don’t even know how long these tariffs will last, no one does, and for that reason alone I won’t be looking to purchase any shares from McRae until these uncertainties clear up.

Disclosure: I do not own shares of either McRae Industries, Inc.’s common stock (Class A ($MCRAA) or Class B ($MCRAB)). This is not financial advice. I am not a financial advisor. Do Your Own Research.